Relationship Intelligence

What Is Relationship Intelligence?

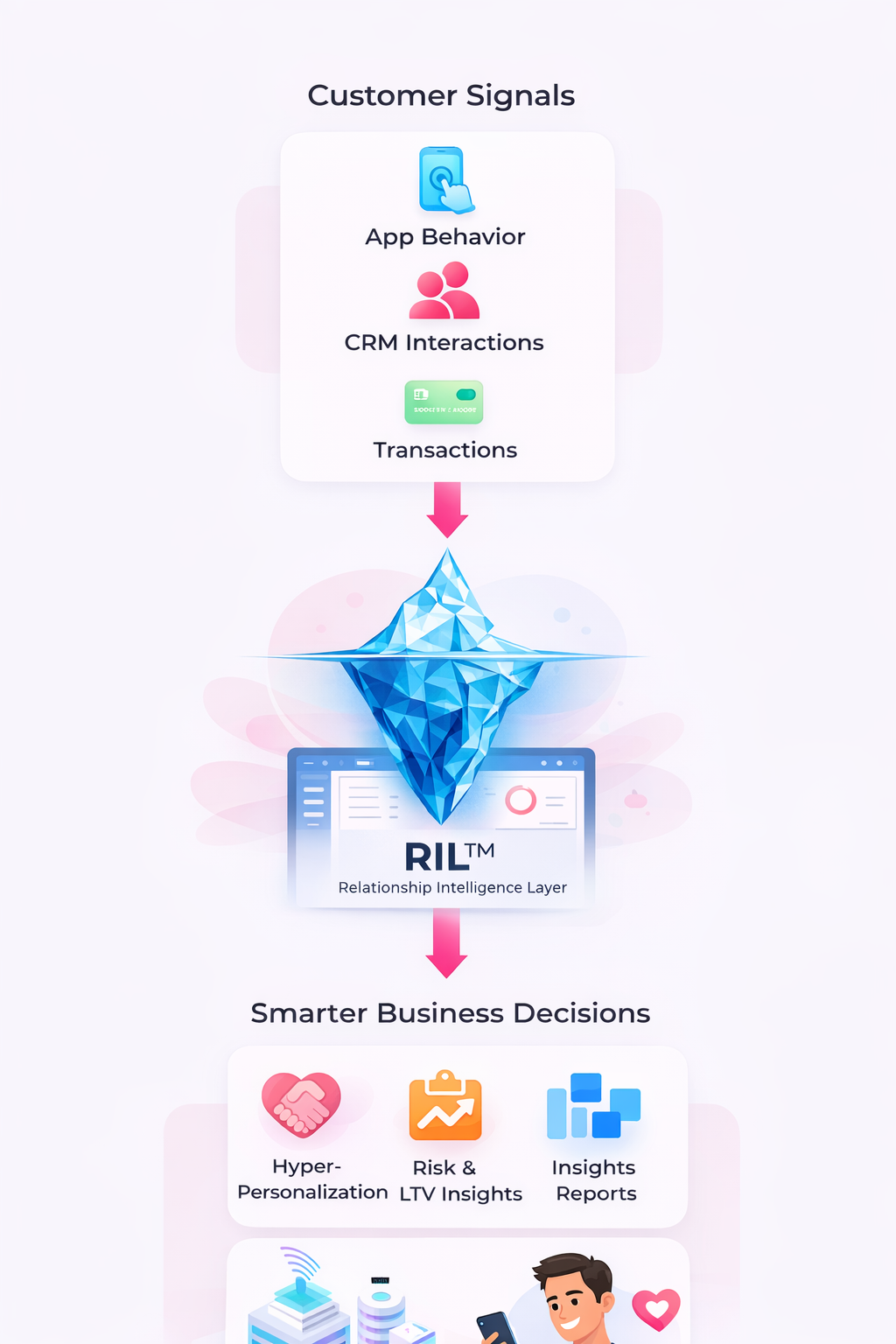

Relationship intelligence infinancial services refers to the ability of financial institutions tounderstand customers not as isolated transactions, but as evolving behavioralrelationships over time.Traditional financial systems werebuilt around events:

a transaction, a payment, a credit application, a fraud alert. Each event wasevaluated separately, often through rule-based models or static risk scoringframeworks.Relationship intelligence shifts theperspective. Instead of analyzing isolated actions, institutions analyzepatterns of interaction across time, channels, and financial contexts.In this model, the relationshipitself becomes the primary unit of analysis.Every action — from spendingbehavior to repayment timing, digital engagement patterns, and response tofinancial stress — contributes to a continuously evolving understanding of thecustomer

The goal is not simply to detectanomalies or trigger offers. It is to build a dynamic model of how therelationship between the institution and the customer evolves.

Why Relationship Intelligence Matters Now

Several structural changes infinancial services make relationship intelligence increasingly important.

Digital financial ecosystems

- Customers now interact withfinancial institutions through multiple channels: mobile banking, embeddedfinance platforms, payment ecosystems, and digital lending environments.

- These interactions generatebehavioral signals that extend far beyond traditional credit bureau data.

Fragmented financial behavior

- Customers often hold accounts acrossmultiple institutions and services.

- Static customer profiles fail to capture how individuals manage liquidity, risk tolerance, and financial prioritiesacross contexts.

- Relationship intelligence enablesinstitutions to detect patterns that emerge only when behavior is observed overtime.

Earlysignals of risk and opportunity

- Financial stress rarely appearssuddenly. It emerges gradually through subtle behavioral shifts: changes inpayment timing, spending volatility, reduced engagement, or increased relianceon credit.

- Systems designed to evaluateisolated transactions often miss these early indicators.

Transitionfrom product-driven to relationship-driven models

- Historically, financial institutionsoptimized around products: loans, accounts, cards, and investments.

- Modern financial ecosystemsincreasingly optimize around relationships — long-term engagement, trust, andlifecycle value.

- Relationship intelligence providesthe analytical layer necessary to support this shift.

Relationship Intelligence provide you with the motivators of your customer that are needed in every interaction

How Relationship Intelligence Works

Conceptually, relationshipintelligence operates through three analytical layers.

Longitudinal Behavioral Analysis

Rather than evaluating individualevents, the system evaluates patterns across time, as:

- In app behavior

- Engagement intensity within digital channels

- Changes in transaction regularity

These patterns reveal behavioral trajectories rather than isolated data points.

Adaptive Relationship Modeling

The relationship between aninstitution and a customer evolves over time.

Adaptive models continuously updatetheir understanding of:

- Trust

- Financial Stability

- Risk Exposure

Rather than recalculating scoresperiodically, the system maintains an ongoing relationship model.

Contextual Interpretation

Behavior rarely has meaning without context.

Behavioral AI matters now because itallows financial institutions to:

- Increased spending may signal financial stress in one context, and normal seasonal activity in another.

- Reduced engagement may reflect satisfaction for one customer and disengagement for another.

- Trust, intent, and vulnerability shift over time

Relationship intelligenceincorporates contextual variables such as timing, historical patterns, andcustomer lifecycle stage.

- React to behavior as it happens

- Detectearly signals before problems escalate

- Build ongoing relationships instead of one-time decisions

Where Traditional Systems Fall Short

Most financial institutions operatewith infrastructure that was not designed to support relationship intelligence.

Common limitations include:

Transaction-centricarchitecture

- Core banking systems and decision engines are optimized for event processing

- Less on longitudinal behavior alanalysis gathered from various sources

Siloed decision environments

- Risk systems, marketing platforms,fraud detection engines, and product analytics often operate independently.

- Each system maintains a partial viewof the customer.

- Relationship intelligence requiresintegration across these domains.

Static riskframeworks

- Traditional credit scoring modelsrely heavily on historical averages and bureau data.

- While valuable, these models oftenfail to capture behavioral dynamics occurring within the institution’s ownecosystem.

Limitedbehavioral interpretation

- Raw behavioral data is frequentlyavailable but underutilized.

- Without behavioral modelingframeworks, institutions struggle to convert signals into actionable insights.

The Role ofBehavioral AI

Relationship Intelignence depends heavily on behavioral interpretation.

Financial behavior is complex.

Customers do not follow static patterns.

Context and change are critical.This is where Behavioral AI becomes foundational.Behavioral AI enables systems tointerpret how actions fit within a broader behavioral trajectory.

Instead of evaluating isolatedevents, behavioral models analyze patterns such as:

- Gradual shifts in financial discipline

- Sudden behavioral anomalies

- Decision timing patterns

- Interaction consistency across channels

A deeper explanation of thisbehavioral infrastructure is explored in our overview of Behavioral AI infinancial services.Relationship intelligence builds onthis layer by applying behavioral understanding across the entire lifecycle ofthe customer relationship.

Relationship Intelligence and Hyper-Personalization

Relationship intelligence also forms the foundation for hyper-personalization in financial services.While hyper-personalization focuseson adapting offers and decisions at the individual level, relationship intelligence provides the longitudinal context necessary to support thoseadaptations. Without understanding the trajectoryof a relationship, personalization risks becoming reactive rather thanstrategic.

A more detailed exploration of thisadaptive personalization model can be found in our discussion of Hyper-Personalizationin Financial Services.Together, these capabilities enableinstitutions to move beyond reactive systems toward adaptiverelationship-driven architectures.

Practical Applications

Relationship intelligence caninfluence multiple areas of financial operations.

Propensity Scoring Models

Predicting LTV, Churn, credit

Likelihood to make a choice

E.g. Credit card activation

Credit Strategy

Builds credit models based on psychology

Does not require transactional history

Adjusting credit exposure dynamically

Customer Engagement

Tailoring communication strategies

Persuasive messaging based on motivators.

Serves also for collection purposes

Customer Data Profiling (CDP)

Integrates with Adobe for Business

Insights report, serve data scientists and marketing teams, creating audiences.

OrganizationalImplications

Adopting relationship intelligencerequires structural changes beyond technology.Financial institutions must align:

- Data Infrastructure

- Risk Governance

- Product Strategy

Decision systems must move fromisolated rule engines to integrated intelligence layers capable of analyzingbehavioral patterns across domains.This transition also raisesimportant ethical and regulatory considerations.Behavioral models must remainexplainable, auditable, and consistent with regulatory expectations regardingfairness and transparency.When implemented responsibly,relationship intelligence strengthens both customer trust and institutionalresilience.

Frequently Asked Questions (FAQ)

Traditional CRM systems track interactions and communication history. Relationship intelligence analyzes behavioral patterns to interpret how financial relationships evolve over time.

No. It complements existing risk models by providing additional behavioral context that can enhance decision accuracy.

No. The concept applies across financial sectors including lending platforms, payments, wealth management, and embedded finance ecosystems.

While some insights can be derived from batch analysis, the full potential of relationship intelligence emerges when behavioral signals are processed continuously.

TheStrategic Shift

Financial systems historicallyoptimized for transactions.

Modern financial ecosystemsincreasingly optimize for relationships.

- Relationship intelligence representsthe analytical framework required to understand those relationships as dynamicsystems rather than static profiles.

- Institutions that adopt thisapproach move beyond reacting to events and begin to anticipate the evolutionof financial behavior.

- This shift will define the nextgeneration of financial decision systems.